INSURANCE APPRAISAL & UMPIRE PROCESS

The Insurance Appraisal & Umpire process is an alternative to court proceedings and works to resolve the differences between the insured and the insurance carrier in an organized, and final process. Policy provisions control when and if it can be invoked as well as the qualification of the appraisers and umpires. Appraisal does not deal with coverage issues and may require court appointment of an umpire if one is not agreed to.

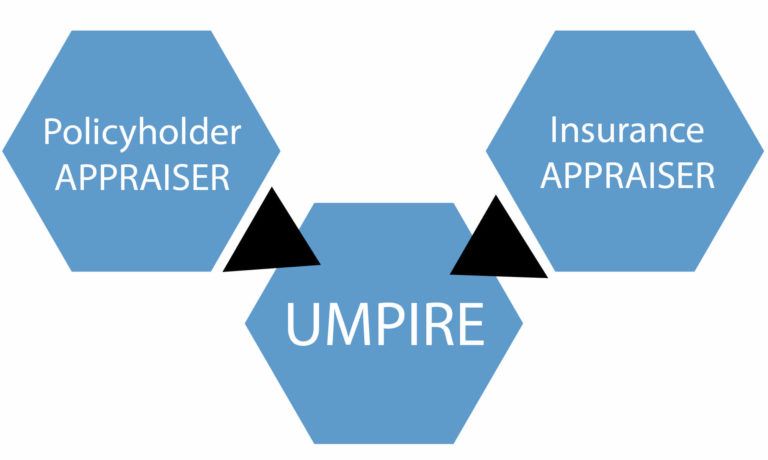

STEP 1- After the initial adjusting between the insured and the carrier, a difference or dispute exists as to VALUE and EXTENT of the LOSS.

STEP 2- The insured and the insurer each select their own appraiser who together select and umpire or the court appoints one.

STEP 3- The two appraisers try to settle their differences to reach a full and fair settlement of the insured’s claim by reviewing the documents, photos, evidence and together conduct a site inspection. If the matter is settled, a mutual award is executed and the matter is resolved.

STEP 4- If the matter is not settled, the Umpire is engaged, who further reviews the documents, photos and evidence and conducts an additional inspection of the property.

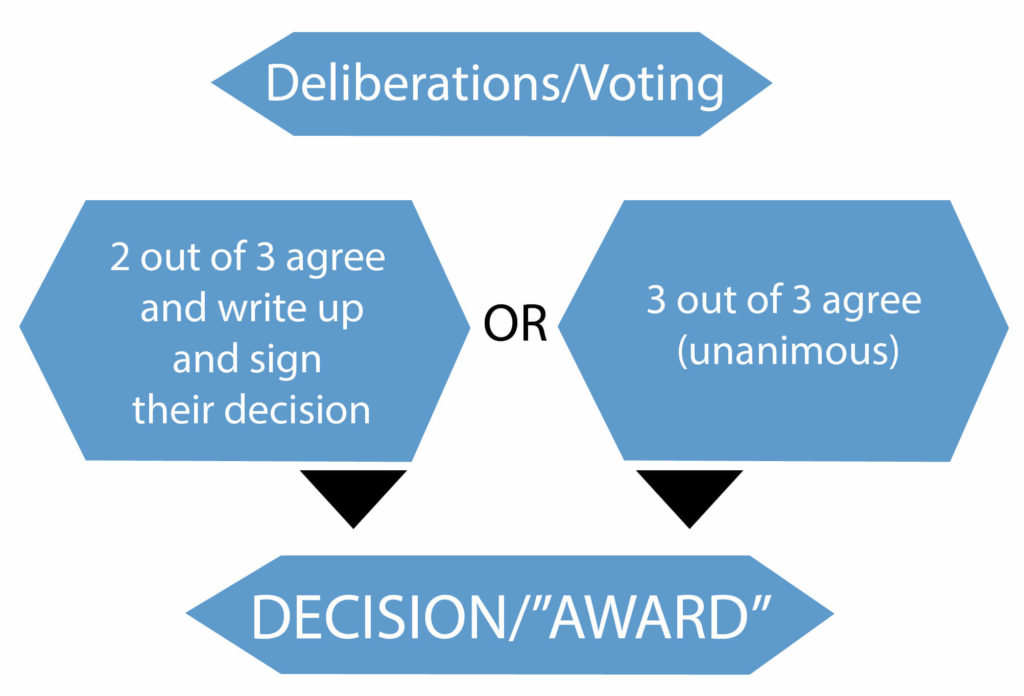

STEP 5- The Umpire independently issues a proposed decision, called an “award”.

STEP 6- When one or both of the appraisers agree with the Umpire’s award, the umpire Award is signed, resulting in payment and enforcement of the award.

The matter is concluded. The award has the effect of a Judgment and is binding on both parties.

Appraisal vs Lawsuit

The appraisal process has several benefits compared to litigation over property insurance losses such as:

A quick, expedient process;

Relatively less costly that litigation;

Because it is less adversarial, it tends to reach equitable resolutions;

It is final, and no appeal is permitted; and

Informal procedures permit creative and just resolution of claims

What is an “Appraisal Clause”?

Appraisal clauses have been a common provision of insurance policies for more than a century, but have only gained acceptance since the 1980’s. Usually appearing in the “CONDITIONS” sections of policies, these provisions are designed to provide a nonjudicial means of resolving disputes between insurers and insureds when the two parties are unable to agree on the amount of money an insurer should pay to settle a claim.

Typical Appraisal Clause in Contracts of Insurance

Although certain carriers and policies under the Federal Flood Insurance Program have specific language, including those regarding the selection of an umpire, generally, policy provisions regarding the invocation of the appraisal process provide:

“APPRAISAL- If you and we fail to agree on the amount of loss, either one can demand that the amount of the loss be set by appraisal. If either makes a written demand for appraisal, each shall select a competent, independent appraiser. Each shall notify the other of the appraiser’s identity within 20 days of receipt of the written demand. The two appraisers shall then select a competent, [disinterested] [impartial] l Umpire. If the two appraisers are unable to agree upon an Umpire within 15 days, you or we can ask a judge of a court of record in the state where the residence premises is located to select an Umpire. The appraisers shall then set the amount of the loss. If the appraisers fail to agree within a reasonable time, they shall submit their differences to the Umpire. Written agreement signed by any two of these three shall et the amount of the loss”.

A typical commercial insurance contract (unless it is a manuscript form) will provide the following language:

“Appraisal If we and you disagree on the value of the property or the amount of loss either may make written demand for an appraisal of the loss. In this event, each party will select a competent and impartial appraiser. The two appraisers will select an umpire. If they cannot agree, either may request that selection be made by a judge of a court having jurisdiction. The appraisers will state separately the value of the property and amount of loss. If they fail to agree, they will submit their differences to the umpire. A decision agreed to by any two will be binding. Each party will:

- Pay its chosen appraiser; and

- Bear the other expenses of the appraisal and umpire equally. If there is an appraisal, we will still retain our right to deny the claim.”AND“The appraisal award must be defined and delineated in such detail so that the loss and damages are described using the following categories:

(1) Actual Cash Value / Replacement Cost Value;(2) Building;

(3) Structures;

(4) Non-covered items and/or excluded items;

(5) Mold and mold remediation;

(6) Contents and personal property;

(7) Cause of loss / cause of peril;

(8) Other expenses;

(9) Business income / extra expense; and

(10) Ordinance or law.”

MANAGED REPAIR PROVISIONS IN HOMEOWNERS POLICIES

Certain Insurance Companies provide appraisal provisions that require the Insured in most instances to utilize a contractor chosen by the carrier, a process known as “Managed Repair” A typical Managed Repair Appraisal Provision provides that:

“Appraisal”. The following is added to the policy:

Where “we” elect to repair: 1. If “you” and “we” fail to agree on the amount of loss, which includes the scope of repairs, either may demand an appraisal as to the amount of loss and the scope of repairs. In this event, each party will choose a competent appraiser within 20 days after receiving a written request from the other. The two appraisers will choose an umpire. If they cannot agree upon an umpire within 15 days, “you” or “we” may request that the choice be made by a judge of a court of record in the state where the “residence premises” is located. The appraisers will separately set the amount of loss and scope of repairs. If the appraisers submit a written report of an agreement to “us”, the amount of loss and scope of repairs agreed upon will be the amount of loss and scope of repairs. If they fail to agree, they will submit their differences to the umpire. A decision agreed to by any two will set the amount of loss and the scope of repairs. Each party will pay its own appraiser, and bear the other expenses of the appraisal and umpire equally.

2. The scope of repairs shall establish the work to be performed and completed by [Carrier’s Preferred Contractor]. Such repair is in lieu of issuing any loss payment to “you” that otherwise would be due under the policy. The amount of loss shall establish only the initial amount paid to [Carrier’s Preferred Contractor”] by “us”, and any additional amounts required to complete repairs shall be Includes copyrighted material of Insurance Services Office, Inc. with its permission “our” responsibility and will be paid to [Carrier’s Preferred Contractor”] without regard to policy limits or the amount of initial payments.

3. If we demanded mediation under Condition G. Mediation of Section I – Conditions and either party rejects the mediation results, “you” are not required to submit to, or participate in, any appraisal of the loss as a precondition to an action against us.”